|

|  |

|  |

| We've detected that you're using an ad content blocking browser plug-in or feature. Ads provide a critical source of revenue to the continued operation of Silicon Investor. We ask that you disable ad blocking while on Silicon Investor in the best interests of our community. If you are not using an ad blocker but are still receiving this message, make sure your browser's tracking protection is set to the 'standard' level. |

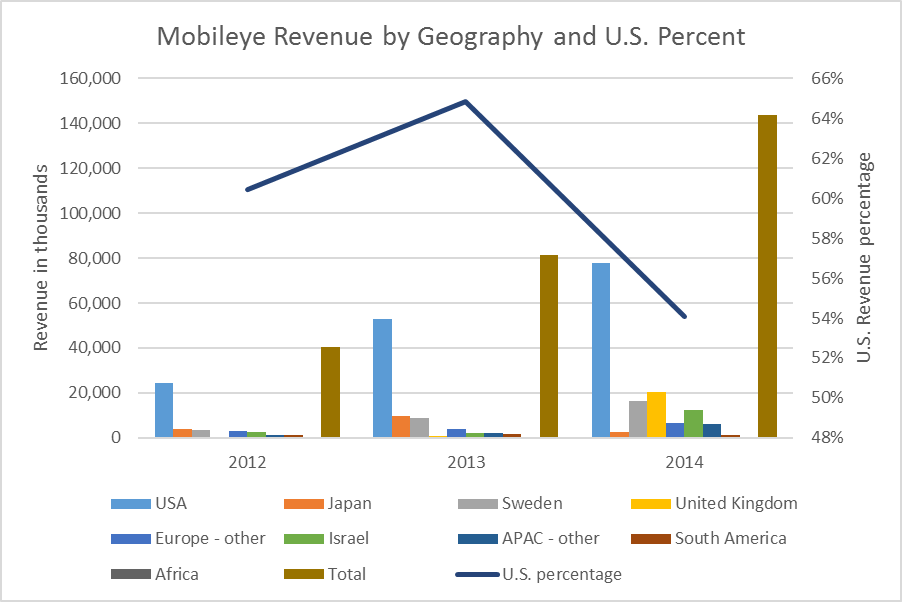

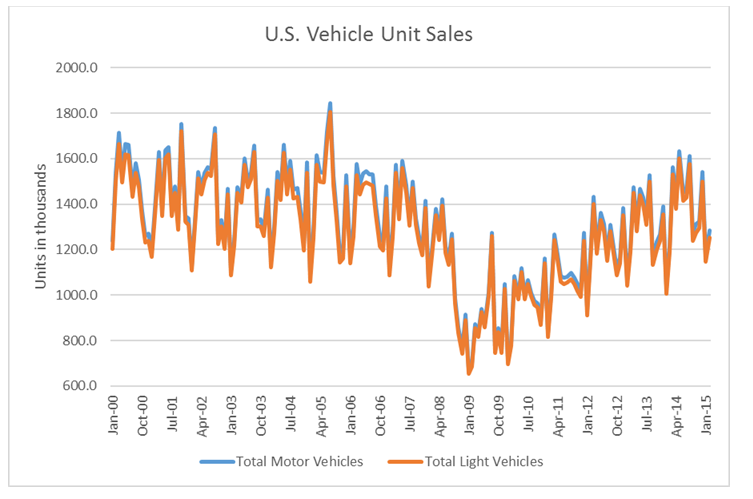

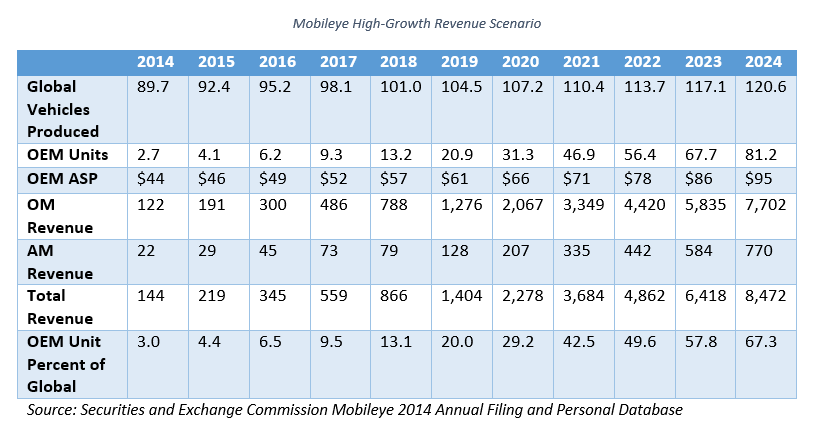

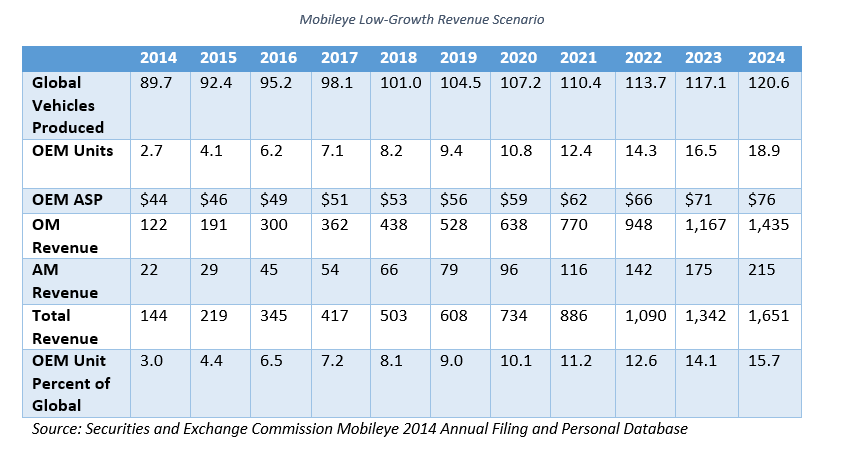

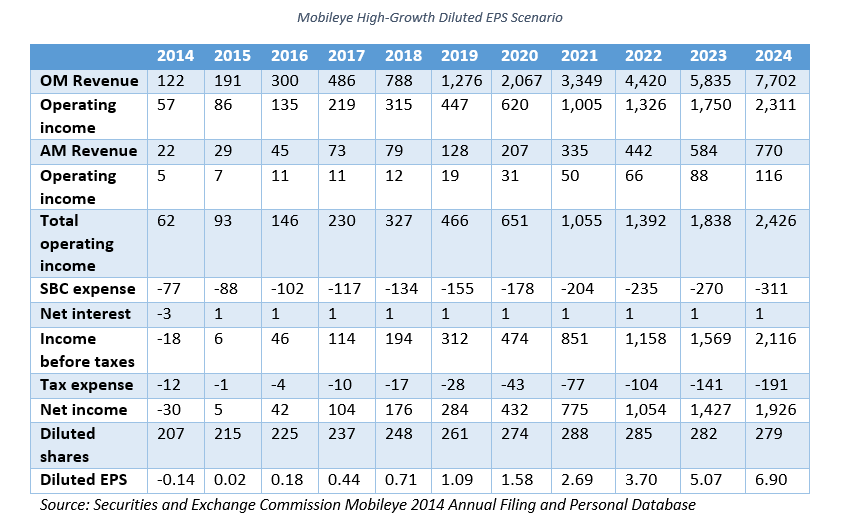

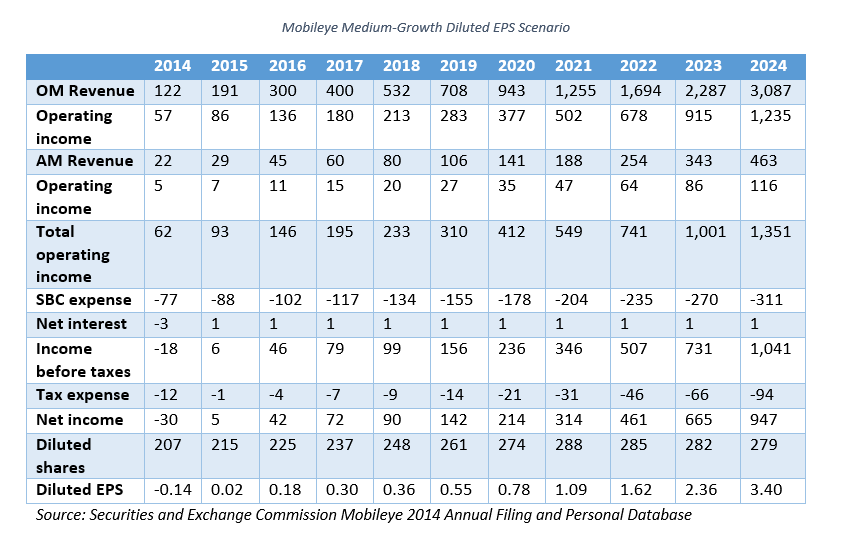

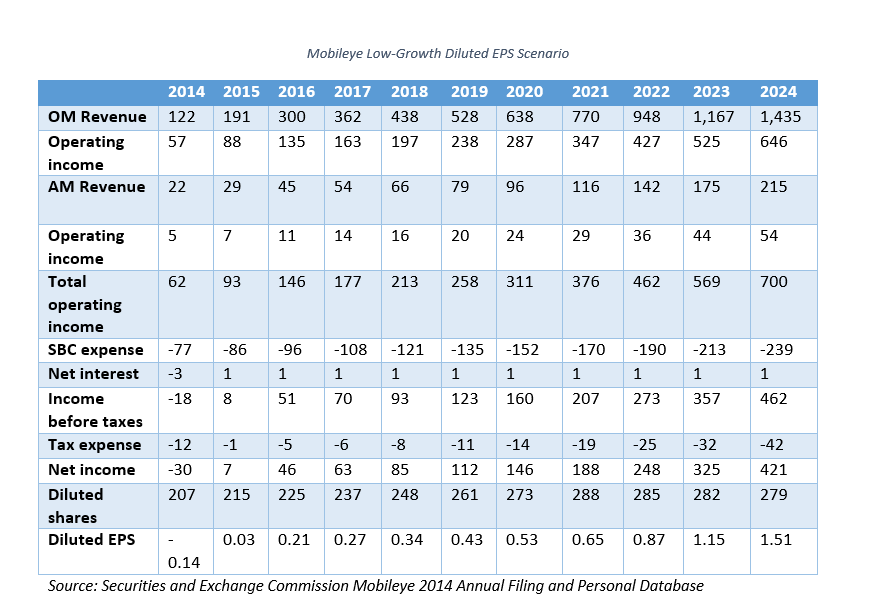

James Sands Long only, portfolio strategy, transportation, growth Profile| Send Message| Follow (474 followers) GOOD ARTICLE .. WORTH THE TIME TO REVIEW...... Mobileye: A Great Investment Opportunity, But At What Price? Mar. 23, 2015 12:11 PM ET | 9 comments | About: Mobileye (MBLY)Subscribers to SA PRO had an early look at this article. Learn more about PRO » Disclosure: The author has no positions in any stocks mentioned, but may initiate a long position in MBLY over the next 72 hours. (More...) SummaryMobileye has positioned itself at the forefront of long-term autonomous vehicle technology growth prospects.The company has executed well as evidenced by a compound annual revenue growth rate of 96% since 2011.Today's $8.9 billion valuation based on enterprise value places high expectations moving forward.Should investors be considering Mobileye's current stock price as an entry point for the long-term? Mobileye N.V. (NYSE: MBLY) is a very interesting company based on the fact that it employs cutting edge technology targeting the evolution of autonomous vehicles. For those not familiar with the term, autonomous vehicles can generally be defined as a vehicle utilizing both visual hardware and technology systems enabling it to self-sufficiently operate without driver control. This of course is not expected to develop immediately as many of us prefer to maintain control over our vehicle operations. But national policies based on safety are interested in reducing accidents to lessen physical injuries and associated costs. As a result safety ratings have become an important standard of which major original equipment manufacturers, or OEMs in the automobile industry have taken notice. This has led to an increasing amount of new technology developments and ultimately to longer-term autonomous vehicle endeavors. For Mobileye, this visual system relies upon the use of cameras, the company's Silicon Core Design EyeQ® chips and technology algorithms to define surrounding environments. Examples are far and wide including recognition of traffic signals, roadway signs, lanes, curb and gutters, pedestrians, bicyclists, construction vehicles, other vehicles, animals, among other transportation-based items and factors. Technology applications for drivers include adaptive cruise control, adaptive high beam control, autonomous emergency braking, or AEB and dynamic brake support, forward collision warning, headway monitoring and warning, lane departure warning, lane keeping, construction zone assistance, among many others. The reason for covering Mobileye is that the company is an innovator and first mover in developing these technologies and has established relationships with OEMs and Tier 1 suppliers. These technologies and applications for vehicles are becoming an increasing reality sooner rather than later. Determining whether Mobileye is a suitable investment for long-term investors seeking growth opportunities is a valid thought. Despite the exciting potential, it is not recommended that investors should jump on this opportunity without considering the details. Mobileye currently stands with an $8.9 billion enterprise value, is not profitable by GAAP, and trades at highly excessive price to book and enterprise value to sales ratios of 24 and 62 times. Mobileye will need to continue to execute in the future, as the next three to five years will be extremely important for the company and automobile industry. Key technology milestones will determine whether project programs are won and directly impact how Mobileye's average selling price, or ASPs per OEM product unit proceeds. For investors, deconstructing and understanding how to interpret the potential for revenue growth and operating and profit margins, should paint enough of a picture as to whether today's price is worth the risk. INVESTMENT THESIS AS THE MARKET IS READING ITMobileye is at the center of the camera-based Advanced Driver Assistance Systems, or ADAS technology. The company believes that as the ADAS market continues to grow, Mobileye's total addressable market will reach $4.5-6 billion annually in the next several years. This assumes that the vast majority of new cars produced will be equipped with one or more ADAS capabilities. In addition, there are an estimated one billion existing automobiles on the road worldwide which could be retrofitted with certain ADAS capabilities. Mobileye believes that other organizations and interest groups, such as insurance companies, fleets and public transportation companies, have shown interest in adapting ADAS to reduce road traffic injuries and damage from collisions; reflecting another growth opportunity in future years. For autonomous driving, Mobileye believes these capabilities will start with hands-free highway driving that will gradually extend to other types of roadways, such as country and city driving. Key factors in the growth of autonomous driving will be increased safety, consumer demand and economic and social benefits. Mobileye believes that the total addressable market for camera-based ADAS systems for autonomous driving could reach $15 billion in the next several years. These market opportunities are being guided heavily by regulations and ratings. In many countries, New Car Assessment Programs, or NCAPs, particularly the European NCAP, and the U.S. NCAP administered by the U.S. National Highway Traffic Safety Administration, or NHTSA, have created a "market for safety." Car manufacturers seek to demonstrate that their new and revamped car models satisfy the NCAP's highest rating, typically five stars, or can "tick the box" on the new car sticker. Europe, the United States, Japan and Australia all have recently implemented policies targeting ADAS capabilities and have near-term policies in place to mandate such capabilities for both ADAS and autonomous vehicle progression. Mobileye has developed a cost-effective camera-based technology, has strong supplier relationships with OEMs, and has substantial validation datasets for complex proprietary algorithms, long-standing relationships with OEMs and Tier 1 direct customers, a self-designed microprocessor chip EyeQ® and a highly scalable business model. To sum things up, Mobileye has provided investors with an enormous opportunity as the company has gone public at an early stage of development. Mobileye generated $143 million in total revenue during 2014. This reflects a 96% annual growth rate since 2011, when the company generated only $19 million in revenue for the year. Our recurring issue throughout this overview will continue to be Mobileye's valuation. In order to get a handle on where the trajectory for the company's business is headed based on valuation, investors need to understand how the company generates revenue through its products and how this in-turn relates to the automobile industry by unit sales. From here growth scenarios can be considered and investors can hopefully decide for themselves at what price risk is merited. Mobileye Revenue Mobileye's revenue can be broken down into two primary segments, OEM and aftermarket, or AM customers. The company has made the following statements: "It took approximately five years from 2007 to ship the first 1.0 million EyeQ® chips. In the year ended December 31, 2014, we shipped approximately 2.7 million chips.""Our ASP grew from $35 to $37 to $44 in the years ended December 31, 2011, 2012 and 2013, respectively.""In 2014, the EyeQ ASP was largely unchanged at approximately $44 because the majority of deliveries were still related to vehicle detection features."This information is highly valuable for investors to deconstruct the company's OEM revenue segment by ASP and units sold. The Mobileye Revenue by Segment and OEM Units Sold figure below displays this. (click to enlarge)  Source: Securities and Exchange Commission Mobileye 2014 Annual Filing and Personal Database In order to get a rough magnitude of the company's units sold we took the OEM revenue divided by the ASP for the years above. Understanding this relationship is important as Mobileye expects to deploy EyeQ3® and EyeQ4® SoCs throughout 2015 and 2018. Each progressive launch of the next generation builds from the previous version allowing for greater functionalities of products for transportation environments, which in turn necessitates more complex algorithms and processing speeds. This progression will lead to higher ASPs for Mobileye. EyeQ3® was recently launched in the fourth quarter of 2014 with one OEM. Nine additional OEM launches are scheduled for 2015 and design wins with three additional OEMs for launches are expected after 2015. EyeQ3® will support full braking AEB, structure from motion functionalities, road profile reconstruction, debris detection, general object detection, and traffic light detection. This chip and technology will also be part of Mobileye's first launch of autonomous driving, expected in 2016.EyeQ4® engineering samples are expected in the fourth quarter of 2015. Mobileye's first design win is from a premium European car manufacturer for serial production in 2018 at a price up to triple the current ASP. This is a result of multiple camera and multifocal sensor functions.As ASPs and units grow over time, the combined affect will translate into robust revenue growth for the company. This is key as the figure above clearly illustrates that the OEM segment is the fastest growing segment driving the majority of the 96% annual growth since 2011. It is also anticipated that as the OEM growth continues that AM customers will similarly see higher ASP and unit growth as the EyeQ3® chip becomes more prevalent within this segment. Addressable Market The Worldwide Automobile Production figure below provides the global supply of vehicles produced since 2000. (click to enlarge)  Source: Statista This figure represents the addressable market for Mobileye as both passenger and commercial vehicles will utilize forms of ADAS and autonomous vehicle technologies. When we consider the 2.7 million OEM units incorporating Mobileye chips during 2014 that the company produced, we can clearly see that this reflects only 3% of the global vehicles produced during 2014. The Growing Number of Contracted Models figure below shows the growth in Mobileye's car model contracts through 2014, and includes the expectations through 2016.  Source: Securities and Exchange Commission Mobileye 2014 Annual Filing This information is valuable because Mobileye has stated that it will take a competitor five to seven years to establish the necessary testing and validation and implementation dynamics to bring an equivalent technology product to market with OEMs and Tier 1 suppliers. For its OEM products Mobileye provides the software and EyeQ® SoC to the Tier 1 companies. Mobileye is responsible for working with OEMs to validate the product prior to an RFQ being submitted; this requires several years of a learning curve. Tier 1 suppliers use Mobileye's reference designs to build a module for the complete sensor system that includes the windshield-mounted camera, Mobileye's EyeQ® SoC and application software using its algorithms. This complete system is then integrated into new cars by the OEM. To date, Mobileye has executed well and experienced robust success based on the company's established relationships with existing Tier 1 suppliers and OEMs. The company has witnessed near 70% annual growth in number of contracted models since 2011. Transitioning this back to revenue, the Mobileye Revenue by Geography and U.S. Percent figure below depicts the recent importance that the U.S. market has played in the company's revenue generation. Geographic revenues are based on the country that Mobileye's product is shipped to. (click to enlarge)  Source: Securities and Exchange Commission Mobileye 2014 Annual Filing and Personal Database While declining during 2014, the U.S. revenue as a percent of the total remained strong at 54%. Other growth trends during the year that were significant include increased proportions for Sweden, the United Kingdom and Israel. Europe - other and the Asia Pacific region or APAC - other both also witnessed increases. This is an important note as the U.S. Vehicle Unit Sales figure below illustrates the uptrend being witnessed for U.S. vehicle unit growth post-recession. From the information it is clear that the U.S. sells a majority of light duty vehicles and not many heavy duty ones. The figure below also clearly displays seasonality. This is of note as Mobileye has yet to witness seasonality, but we should anticipate it to occur. As the company scales it should begin to mirror vehicle unit sales. (click to enlarge)  Source: Bureau of Economic Analysis and Personal Database During 2014, the U.S. unit sales totaled roughly 16.8 million. If we use rough comparisons for Mobileye's revenue geography of 54% for U.S. revenue and apply it to the 2.7 million OEM units, we get around 1.5 million units for the U.S. This equates to a 9% share of the market. When considering the number of global vehicles produced and the penetration that Mobileye has been able to make to date, there are vast opportunities moving forward. GROWTH POTENTIAL SCENARIOSThe information we have is not perfect, but it should be good enough to think about Mobileye's valuation and growth potential. Between 2012 and 2014 Mobileye has witnessed OEM product unit growth of 91% per year. Since the ASP for the company was flat during 2014, the average ASP growth since 2011 has been 8% per year. It should be noted that these growth rates do not reflect what will happen next year necessarily or over the next ten years for that matter. Additionally, we do not have a good way to measure the AM segment. The only information we know regarding the AM segment is that the company realizes a higher ASP when directly selling to customers versus through distributors; and that the average ASP declined 2% from 2013 to 2014. But we should assume that retrofitting will increase as ADAS and autonomous vehicles become more prevalent in global markets. Additionally upgrades for EyeQ3® chips and subsequent products into the AM market will occur. As a result, our OEM baseline is 2.7 million product units sold in 2014 at an ASP of $44/unit. For the AM segment, we can either attempt to assume a proportional relationship to the OEM segment or project out assumed growth rates from general AM revenue trends. Neither one is preferred but I would rather use OEM as a peg and assume that over the next three years, AM will represent 15% of OEM. From thereon I will place it near 10%. These should reflect conservative estimates as AM currently represents 19% of OEM revenues. The three tables below reflect high, medium and low growth assumptions for OEM units and ASP and include the assumptions as stated above for the AM segment. Global vehicles produced, OEM units and revenue line items are expressed in millions. It should be noted that all scenarios assume the same assumptions through 2016 and are in-line with average analyst estimates. Global vehicles produced assumes an average growth rate of 3% per year reflecting the most recent trend between 2007 and 2014 accounting for the recession. (click to enlarge)  For the high-growth scenario the following assumptions were made: OEM unit growth of 50% per year through 2021, and 20% per year thereafterOEM ASP growth of 5% per year through 2016, and 8-10% per year thereafterUnder a high-growth scenario Mobileye is estimated to grow OEM unit production by 41% per year over the next decade leading to $8.5 billion in total revenue earned and a 67% global market share by 2024 of vehicles produced. This compares to a 91% OEM unit production per year growth rate between 2012 and 2014. The ASP doubles by 2024 as well; management has stated that EyeQ4® chips may receive up to triple the current ASP once launched. (click to enlarge)  For the medium-growth scenario the following assumptions were made: OEM unit growth of 50% per year through 2016, and 25%per year thereafterOEM ASP growth of 5% per year through 2016, and 6.5-8%per year thereafterUnder a medium-growth scenario Mobileye is estimated to grow OEM unit production by 30% per year over the next decade leading to $3.6 billion in total revenue earned and a 31% global market share by 2024 of vehicles produced. This scenario reflects robust growth at a slower pace when compared to the high-growth scenario; and OEM ASP does not double over the long-term. (click to enlarge)  For the low-growth scenario the following assumptions were made: OEM unit growth of 50% per year through 2016, and 15%per year thereafterOEM ASP growth of 5% per year through 2021, and 7%per year thereafterUnder a low-growth scenario Mobileye is estimated to grow OEM unit production by 21% per year over the next decade leading to $1.7 billion in total revenue earned and a 16% global market share by 2024 of vehicles produced. Under a scenario like this it would most likely be assumed that other technologies have become competitive hampering growth. From these three growth scenarios it is clear to see that in the low-growth scenario, Mobileye could not offer substantial value today when considering an enterprise value to sales multiple near 5.2 times 2024 total revenue at today's $8.9 billion enterprise value. Compared to the high- and low-growth scenarios the same multiple would be 1.0 and 2.5 respectively. It is not uncommon for growth companies to command EV/sales multiples of 5-7 times. In the high- and mid-growth scenarios more upside potential is offered over the long-term. Irrespective of top-line growth, Mobileye's business model has placed the company in an advantageous position for profitability. Mobileye during 2014 had an operating margin for the OEM segment near 45% and 25% for the AM segment. The next high, medium and low growth scenarios will compare the remaining expenses to estimate diluted earnings per share, or EPS. To be conservative for the high-growth scenario the 45% assumption will be carried through 2017 and eventually decline to a 30% margin by 2024. This assumes higher expenses for growth. The mid-growth scenario assumes the same, but the decline is only to 40% by 2024; while the low-growth scenario assumes constant 45% margins. These margins did not include share-based compensation, or SBC. It should be noted that the company reports non-GAAP adjusted net income which excludes SBC and is considered an internal operating metric. Regardless, we can take these assumptions and apply them to our high, medium and low revenue growth scenarios, and then factor out SBC expense, net interest and the effective tax rate. Management expects revenue growth to significantly outpace operating expense growth excluding SBC. The tables below provide high, medium and low diluted EPS scenarios. This helps to further develop an understanding of valuation multiples for Mobileye's stock price today versus its long-term potential. The assumptions above for OEM and AM operating margins are included, as well as a 15% annual growth rate for SBC for the high- and medium-growth scenarios and a 12% annual growth rate for SBC for the low-growth scenario. The ramp-up for SBC expenses leading to extreme operating expense increases during 2014 is not anticipated to continue at the same rate as this was purely related to the company transitioning to a public entity. Net interest is kept constant at $1 million from 2015 and afterward, and the effective tax rate is assumed at 9% per the Israel tax statute disclosures in the annual filing. If Mobileye does not meet certain requirements, the effective tax rate may be anywhere between 10-20%. Diluted earnings per share are expected to increase by 5% per year until 2021, and are expected to marginally decline thereafter. All line items below are expressed in millions, except diluted EPS information. (click to enlarge)  In the high-growth scenario, Mobileye is estimated to generate 6.90/diluted EPS. This would give the company a P/E ratio today of 6.3 times 2024 earnings based on a stock price of $43.27/share. The problem is that in the near-term the P/E ratio is much larger at 239 times 2016 earnings. Assuming a P/E ratio around 30 times earnings in 2024 would equate to a stock price of $207/share. This would generate an annualized return of 17% per year with a market capitalization of $58 billion and a price to sales of 6.8 times. It would appear that in the event Mobileye is able to achieve excessively robust OEM unit growth to a significant market share over the long-term, that today's stock price could possibly merit a good entry. That being said, investors would be forced to take on a lot of risk based on the P/E expectations for this year through 2020. However, if Mobileye is able to beat estimates and increase growth in the near-term hinting towards this type of scenario, the stock price could move higher from today's levels as well. (click to enlarge)  In the medium-growth scenario, Mobileye is estimated to generate 3.40/diluted EPS. This would give the company a P/E ratio today of 12.7 times 2024 earnings based on a stock price of $43.27/share. Again the near-term P/E ratio stands out as excessive for 2016. Assuming a P/E ratio around 30 times earnings in 2024 would equate to a stock price of $102/share. This would generate an annualized return of 9% with a market capitalization of $28 billion and a price to sales of 7.8 times. For this scenario, the rate of return of 9% is a decent return, but may not merit the risk in my opinion. There are many companies in the investment world where investors could attempt to get this type of return at a much lower risk level. (click to enlarge)  In the low-growth scenario, Mobileye is estimated to generate 1.51/diluted EPS. This would give the company a P/E ratio today of 28.7 times 2024 earnings based on a stock price of $43.27/share. Assuming a P/E ratio around 30 times earnings in 2024 would equate to a stock price of $45/share; leading to an annual return of 0.5% per year through 2024. This would generate a minimal annualized return with a market capitalization of $12.6 billion and a price to sales of 7.4 times. For this scenario, it is obvious that today's price does not merit the risk. It should be noted that this scenario would most likely mean that competition would become significant by 2017 impacting growth. Investors would be well-suited to wait for a pull-back to the $20/share range in this environment. Summary So some might ask, why use a P/E ratio of 30 times earnings as a long-term assumption. This is a reasonable premium to assume for an innovative company that will grow over the long-term. The market at certain time periods may give Mobileye a P/E ratio of 200, 500 or even 700; by 2024 the P/E may be 50 or 20. For growth companies, 30 gives us something in the middle of what is reasonable. An important caveat for this exercise is that real world factors affecting these scenarios will pretty much ensure that what is on the tables above does not play out. Long-term projections are not meant to act as "claim-to-fame" estimates where one day, I just may be right on. They rather serve as bookends or high-level guides, so we can get a sense of today's value relative to tomorrow's potential. From this exercise, investors should have a clear focus for Mobileye's prospects. The fact that the company expects its revenue growth to outpace non-GAAP operating margins is our first important note. Again, this excludes SBC, but we should continue to assess the rate of revenue growth versus the rate of non-GAAP operating profit growth. Any deviation should raise a question as to the business model. The catalysts for this expected revenue growth outperformance are that OEM product units will continue to grow at a higher rate due to OEM design wins, product launches and eventual autonomous products for EyeQ3® and EyeQ4® chips. These product developments will also increase the ASP providing for further growth in OEM and AM segments. This is great and should continue to growth the company through 2020, but newer product launches will be expected for growth to continue through 2025 and afterward. By focusing on the company's quarterly updates and getting this information we can continue to tweak our near-term estimates and update the long-term potential scenarios. This is the balance that most analysts are tasked with performing; keeping both the near-term and long-term perspectives in place as things change. The tables above provide baseline, near-term and long-term information. Distilling management's guidance and presentation of information is crucial in interpreting changes in the company's operations and results. OBSTACLES TO GROWTH POTENTIALIt makes sense to also think about the obstacles to the growth potential for Mobileye. The company provides its risks and competition sections in the filings, but is pretty firm with its stance of having a high-barrier competitive product and process. This places more pressure for investors to look for reasonable and important obstacles in the way of the business model. While there are always many risks to any business including management longevity, economic cycles, and many others, for Mobileye key factors to focus on include competition and technology innovation. All investors should review the risks disclosed in Mobileye's 2014 annual filing. Mobileye states that the primary competitors the company faces are Tier 1 suppliers and other technology companies. To put this into perspective, Tier 1 supplier companies provide many different OEM product needs, of which safety-based products are included. Other technology companies is a broad statement. We all know that Google, Inc. (NASDAQ: GOOG) has been developing autonomous vehicles and that all of Mobileye's EyeQ® integrated circuits are manufactured by STMicroelectronics N.V. (NYSE: STM). So to fully understand the competitive environment, Mobileye is engaged with both Tier 1 suppliers and STM throughout its course of regular business. Mobileye does not have exclusive long-term contract agreements with Tier 1 suppliers. The company does have longer-term contracts with STM and there are non-compete provisions once these contracts run out for a short-term time period. Basically there is nothing precluding Tier 1 suppliers or STM or other chip manufacturer companies to compete with Mobileye. That being said, Mobileye's position is that they are seeing Tier 1 suppliers lessen their work efforts on this technology other than the camera-based hardware modules to support the chips and software. Mobileye also states that the company does not work with Tier 1 suppliers who offer competitive products. Mobileye is also in the process of looking to add another chip manufacturer to supply its needs. The contract termination date for STM is December 2022. We have not seen major announcements regarding Google and OEM or Tier 1 suppliers much, so Mobileye's claim that the five to seven year timeframe to bring a product to launch may have merit. This has also been espoused by analysts. But the key thing to pay attention to is Mobileye's action related to Tier 1 suppliers. The market is already wise to this as we consider recent stock price volatility based on the fact that France's Valeo recently agreed to incorporate Mobileye products. On the flip side, information was also recently published regarding Freescale (NYSE: FSL) entering into the market through support for radar, lidar, ultrasonic information, and other data systems becoming available in July. In both situations, the stock price was highly sensitive correlating positively and negatively to the news. It should be assumed that each Tier 1 supplier win adds another potential competitor to Mobileye's defense, and that any loss of Tier 1 suppliers creates an immediate potential threat. This brings us to our second possible obstacle, technology and innovation. Mobileye has sold its proposition to investors and the automobile industry that using a camera module as a "data system collector" is the best method for technology chip and software application processing rather than going with radar, lidar or other systems independently. Investors need to understand that both radar and lidar have been included as ADAS applications in vehicles. There are limitations for both which Mobileye explains within its annual filing, which include detection limitations, false reaction scenarios, and higher costs among others. There are potential scenarios where multiple cameras may be used, and/or the fusion or use of multiple sensors may be incorporated. What is understood by the actions taken recently by Freescale is that the market opportunity will encourage more entrants to compete by focusing on alternative technologies. This is both good and bad as many companies will most likely not make much progress and possibly fail, but a few may come up with alternative solutions that are cost-effective over time. Moving forward, these testing results of other technologies need to be monitored on the level of products provided versus the cost in comparison to Mobileye's system. CONCLUSIONUpon the review of Mobileye, it is definitely a company that I would like to add to the Individual Investor Portfolio, or IIP. However, I am struggling with the valuation of the company as it sits today. What we can gather from the growth potential scenarios is that if Mobileye is highly successful over time, the company could potentially offer investors very robust returns from today's price. However, if a position is entered today, there will be significant risk in both the near-term and long-term for investors. Thus, the first proposition is always to ensure that risk tolerances are in place to even consider such a position. For the IIP portfolio risk-taking is part of the objective. The justification for considering Mobileye is that the automobile industry is going to see technology shifts towards safer vehicles in the next few years, and that this should only intensify more over time. As Mobileye has attempted to measure the market potential in the near-term, there may be multiple companies who will benefit in the eventual greater than $6 billion per year opportunity. The lowest stock price that Mobileye has closed at since going public is $32.15/share. This reflects a 26% decrease from today's price of $43.27/share. The highest stock price that Mobileye has closed at since going public is $57.70/share, reflecting a 33% premium to today's price. On March 2nd, Mobileye closed at $33.66/share. According to Yahoo! Finance, average analyst estimates are at $55.22/share over the next year. This past Friday, Mobileye displayed that it is not necessarily going to trade with the market momentum. I would prefer this to be the case, and would look to be a little patient and possibly enter a position under $40/share. In my opinion, Mobileye is a company whose prospects can change quite rapidly based on the many events mentioned earlier. For these reasons and depending on investor risk tolerances, I believe that Mobileye merits consideration. Based on this I am looking to initiate a 25% portion of available cash for adding Mobileye to the IIP portfolio in the near-term. | ||||||||||||||

|

| Home | Hot | SubjectMarks | PeopleMarks | Keepers | Settings |

| Terms Of Use | Contact Us | Copyright/IP Policy | Privacy Policy | About Us | FAQ | Advertise on SI |

| © 2025 Knight Sac Media. Data provided by Twelve Data, Alpha Vantage, and CityFALCON News |