Overview Of Agriculture Sector In Malaysia

- 1. OVERVIEW OF THE AGRICULTURE SECTOR IN MALAYSIA

- 2. Map of Malaysia SARAWAK SABAH PENINSULAR

- 3. Total land area - 33 million ha. Agricultural area - 6.6 million ha (20% of total area) Industrial crops - oil palm, rubber, cocoa, tobacco and pepper – occupy about 77% of total agricultural land Other crops - paddy, fruits, vegetables & coconut – cover 16% of total agricultural land Scenario of Malaysian Agriculture

- 4. Agriculture sector in Malaysia is divided into :- (i) Estate sub-sector holdings more than 100 acres (40.5 ha) highly commercialized and efficiently managed owned by private companies, public-listed corporate entities or public land development agencies totally involved in the production of industrial crops such as oil palm, rubber, cocoa and pineapples

- 5. (ii) Smallholders’ sub-sector average farm size is about 1.45 ha and owned by individual farmers collective acreage of land operated by 1,033,065 farmers amounting to 75% of the total area under agriculture less commercialized and less efficiently managed main contributors to food crop production as well as industrial crop production Agriculture sector in Malaysia is divided into :-

- 6. Farmers’ Profile Total Number of Farmers : approximately 1 million * Paddy : + 400,000 Horticultural crop : + 200,000 (Fruits, vegetables, floriculture) Industrial Crops : + 750,000 (Rubber, oil palm) Other Crops : + 50,000 * Some farmers are involved in more than 1 crop

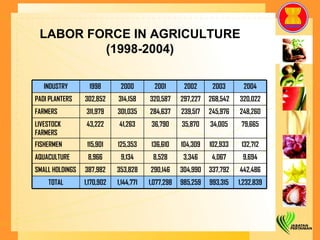

- 7. LABOR FORCE IN AGRICULTURE (1998-2004) INDUSTRY 1998 2000 2001 2002 2003 2004 PADI PLANTERS 302,852 314,158 320,587 297,227 268,542 320,022 FARMERS 311,979 301,035 284,637 239,517 245,976 248,260 LIVESTOCK FARMERS 43,222 41,263 36,790 35,870 34,005 79,665 FISHERMEN 115,901 125,353 136,610 104,309 102,933 132,712 AQUACULTURE 8,966 9,134 8,528 3,346 4,067 9,694 SMALL HOLDINGS 387,982 353,828 290,146 304,990 337,792 442,486 TOTAL 1,170,902 1,144,771 1,077,298 985,259 993,315 1,232,839

- 8. Farmers’ Profile < 45 years old : 30% 45-55 years old : 25 % > 55 years old : 45%

- 9. SCENARIO OF THE NATIONAL AGRICULTURAL SECTOR After Independent: Malaysian an agricultural nation Economic activity over dependant on agriculture & mining Contribution to GDP, 1957: agricultural sector = 46% Total work force, 1966: agricultural sector = 80.3% “ New Millennium” Era Malaysian well known as producer of manufacturing products Contribution to GDP, 2003: agricultural sector = 8.45% Total work force, 2003: agricultural sector = 14.3%

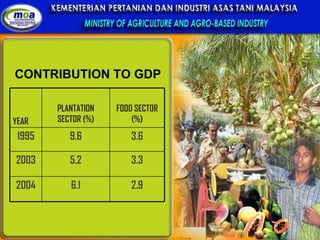

- 10. CONTRIBUTION TO GDP YEAR PLANTATION SECTOR (%) FOOD SECTOR (%) 1995 9.6 3.6 2003 5.2 3.3 2004 6.1 2.9

- 11. AGRICULTURE SECTOR IN MALAYSIA (2006) GDP National= USD 133.8 million Agriculture= USD 11.6 million (8.7%) Trade Export Import National USD 144.3 millon USD 117.3 million Agriculture USD 16.3 million (11%) USD 8.8 million (7.5%) Agro-food USD 2.7 million (1.9%) USD 4.8 milion (4.1%) Labor Force National = 10.5 million person Agriculture = 1.5 million (14.6%)

- 12. AGRICULTURE SECTOR IN MALAYSIA Food Subsector Crop Livestock Fisheries Industrial Commodities Palm Oil Rubber Cocoa Wood & Timber Pepper Agriculture Sector MINISTRY OF AGRICULTURE & AGRO-BASED INDUSTRY MINISTRY OF PRIMARY INDUSTRY & COMMODITIES

- 13. MINISTRY OF AGRICULTURE AND AGRO-BASED INDUSTRY DEPARTMENT OF AGRICULTURE MALAYSIAN AGRI. RESEARCH & DEVELOPMENT INSTITUTE (MARDI) FEDERAL AGRI. MARKETING AUTHORITY (FAMA) MUDA AGRI. DEVELOPMENT AUTHORITY (MADA) KEMUBU AGRI. DEVELOPMENT AUTHORITY (KADA) DEPARTMENT OF VETERINARY SERVICES DEPARTMENT OF FISHERIES MALAYSIA AGRICULTURE BANK (BPM) FARMERS’ ORGANIZATION AUTHORITY (FOA) MALAYSIAN FISHERY DEVELOPMENT BOARD (LKIM) MALAYSIAN PINEAPPLE INDUSTRY DEVELOPMENT BOARD (MPIB)

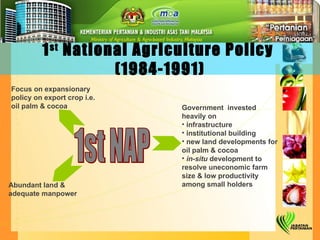

- 15. National Agricultural Policy (Background) Since 1984, three National Agricultural Policy (NAP) were formulated to develop the agricultural sector: Emphasis on NAP1 (1984-1991):- To develop the export oriented sector Current situation : abundant labor force expansionary economic policy adequate land resources commodity/ plantation (palm oil/ cocoa) infrastructure

- 16. 1 st National Agriculture Policy (1984-1991) Focus on expansionary policy on export crop i.e. oil palm & cocoa Abundant land & adequate manpower Government invested heavily on infrastructure institutional building new land developments for oil palm & cocoa in-situ development to resolve uneconomic farm size & low productivity among small holders 1st NAP

- 17. Emphasis of NAP 2 (1992-1997): Increasing productivity, efficiency & competitiveness Increasing land areas for palm oil (plantation crop) Development of agro-based industry National Agricultural Policy (Background)

- 18. Greater focus on issues of productivity, efficiency & competitiveness Addressing the linkages with other economy sector 2 nd National Agriculture Policy (1992-1998) 2nd NAP Shifted from new area development to in-situ development

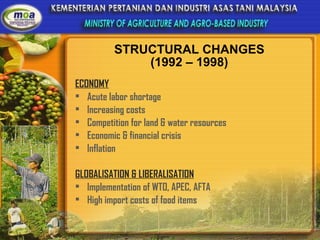

- 19. STRUCTURAL CHANGES (1992 – 1998) ECONOMY Acute labor shortage Increasing costs Competition for land & water resources Economic & financial crisis Inflation GLOBALISATION & LIBERALISATION Implementation of WTO, APEC, AFTA High import costs of food items

- 20. Emphasis of NAP 3 (1998-2010): Increasing the competitiveness of the agricultural sector Maximizing income through : Optimum utilization of resources Increasing agriculture contribution to national GDP Increasing income of producers National Agricultural Policy (Background)

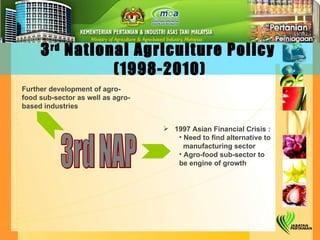

- 21. 3rd NAP Further development of agro-food sub-sector as well as agro-based industries 1997 Asian Financial Crisis : Need to find alternative to manufacturing sector Agro-food sub-sector to be engine of growth 3 rd National Agriculture Policy (1998-2010)

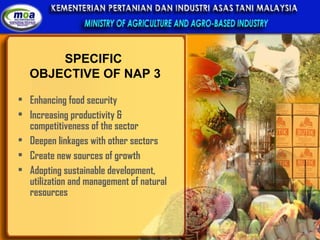

- 22. SPECIFIC OBJECTIVE OF NAP 3 Enhancing food security Increasing productivity & competitiveness of the sector Deepen linkages with other sectors Create new sources of growth Adopting sustainable development, utilization and management of natural resources

- 23. 9 th MP (2006-2010) TARGETS To Increased Value Added Increased Production To Contain Import Bill Increase Self- Sufficiency Level

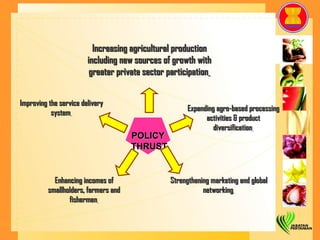

- 24. Increasing agricultural production including new sources of growth with greater private sector participation Improving the service delivery system POLICY THRUST Expanding agro-based processing activities & product diversification Strengthening marketing and global networking Enhancing incomes of smallholders, farmers and fishermen

- 25. DEVELOPMENT OF NATIONAL AGRICULTURAL SECTOR (ISSUES & CHALLENGES)

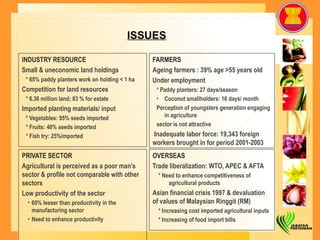

- 26. ISSUES INDUSTRY RESOURCE Small & uneconomic land holdings * 65% paddy planters work on holding < 1 ha Competition for land resources * 6.36 million land; 83 % for estate Imported planting materials/ input * Vegetables: 95% seeds imported * Fruits: 40% seeds imported * Fish try: 25%imported FARMERS Ageing farmers : 39% age >55 years old Under employment * Paddy planters: 27 days/season Coconut smallholders: 16 days/ month Perception of youngsters generation engaging in agriculture sector is not attractive Inadequate labor force: 19,343 foreign workers brought in for period 2001-2003 PRIVATE SECTOR Agricultural is perceived as a poor man’s sector & profile not comparable with other sectors Low productivity of the sector 60% lesser than productivity in the manufacturing sector Need to enhance productivity OVERSEAS Trade liberalization: WTO, APEC & AFTA * Need to enhance competitiveness of agricultural products Asian financial crisis 1997 & devaluation of values of Malaysian Ringgit (RM) * Increasing cost imported agricultural inputs * Increasing of food import bills

- 27. CHALLENGES Transforming small scale agro-industry into commercial ventures Ensuring adequate, quality, safe and nutritious food at a reasonable price Reducing full dependency on labor force in the agricultural sector Ensuring sustainable development of the agricultural sector Increasing competitiveness of the national agricultural sector Strengthening the development of industry in agriculture and of industry in agriculture and to encourage private sector investment

- 28. CHALLENGES To make Agricultural sector as the 3 rd engine of national economic growth (new source) New scope includes agro-based industry Development of the sector covers the total aspect of production and supply chain management

- 29. TRANSFORMING THE AGRI-FOOD SECTOR IN NEW ERA

- 30. Transformation of agriculture and agro-based industry as a sector which is : Modern, Dynamic, and Competitive

- 31. Scope of Transformation Current situation After transformation Farm size: - small Large scale, commercial & economic - uneconomic Labor force: - limited Mechanization, automation & technology - ageing Less labor intensive activities Farm management: Professional, agriculture is business, - traditional Application of ICT, - “satisfactory” Commercial management/ - “enough” collective/economic of scale, - manual Business Plan

- 32. Scope of Transformation Current situation After transformation Less/ not competitive: - Low product quality Standard, certification & - non-standard quality export quality - product dumping - price factor Return on Investment - Low Diversified returns: - time consuming mixed farming, intercropping value-added

- 33. TRANSFORMATION Transformation of Traditional Farmers Sectoral Transformation Land/farm size - Development based on zoning/ cluster Application of technology - Private sector investment Mechanization - Investment incentives Productivity - Implementation of Good Agricultural Supply-demand matching Practices Program (GAP) Marketing Farmer Cooperation Diversity of economic activity Modernization Horizontal/Vertical Transformation - Food processing - Value added activities - supply chain activities - by products

- 34. Transformation of Traditional Farmers Land/farm size : Development of collective agricultural projects ( in-group ) Amalgamation of farms towards creating commercial farm size ( sizeable estates) Introducing systematic & modern farming practices Practicing standard manual- (technology package, business plan & centralized management)

- 35. Transformation of Traditional Farmers Application of technology : Research & Development based on current needs Commercialization & transfer of technology (TOT) Extension programs on technology & training On-site training

- 36. Transformation of Traditional Farmers Reducing labor force in agriculture through : Reduction on labor intensive industries Promoting cultivation of new crops Promoting the production of environmentally controlled systems using mechanization and automation Accelerating R&D in creating new technology that reduces dependency on use of manpower/labor

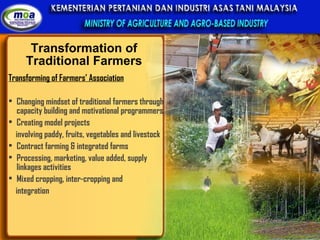

- 37. Transformation of Traditional Farmers Transforming of Farmers’ Association Changing mindset of traditional farmers through capacity building and motivational programmers Creating model projects involving paddy, fruits, vegetables and livestock Contract farming & integrated farms Processing, marketing, value added, supply linkages activities Mixed cropping, inter-cropping and integration

- 38. Transformation of Traditional Farmers Transforming of National Fisherman’s Association Fund for Fishermen Program Use of fishing boats/ vessel and modern fishing equipments Skills enhancement through training and motivational program Branding & collection centre New market opportunities – fish mart, fish kiosk, fish on wheel & in petrol kiosk Inviting giant companies to establish grand seafood restaurant with all modern facilities-as a model

- 39. Transformation of Traditional Farmers QUALITY AND FOOD SAFETY Accreditation and certification program : Producing safe and high quality food Producing food conforms to international standards Promoting sustainable agricultural development

- 40. Farm Accreditation Scheme (Skim Amalan Ladang Baik Malaysia or SALM) Aqua Farm Certification Scheme (Skim Pensijilan Ladang Akuakultur Malaysia SPLAM)

- 41. Farm Accreditation Scheme Malaysia (SALM) Concept of SALM : Inspection and verification of farm by independent auditors Audit for conformance to accepted and defined protocols, national guidelines, standards, legislation and policies. Corrective and preventive actions by farm Benchmarking on specific farm based on EUREGAP, CODEX, others

- 42. Farm Accreditation Scheme Malaysia (SALM) Program to recognize farms that adopt : Good agricultural practices Operates sustainable and environment friendly Safe and quality produce for consumption

- 45. Livestock Accreditation Scheme (Skim Amalan Ladang Ternakan or SALT) (Veterinary Health Mark or VHM) – Processed products DEPARTMENT OF VETERINARY SERVICES, MALAYSIA EST. NO. : …....

- 46. Transformation of Traditional Farmers Marketing Packaging, labeling and branding Conformance to Food Act 1974 Conformance to food safety and sanitation Standard and quality

- 47. Quality Control System (MARDI QAS)

- 48. Seal of Quality Promotion of Malaysian agricultural products through branding

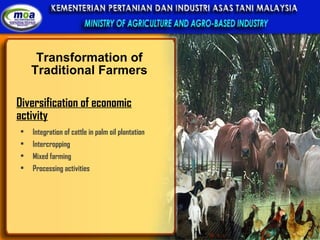

- 49. Transformation of Traditional Farmers Diversification of economic activity Integration of cattle in palm oil plantation Intercropping Mixed farming Processing activities

- 50. Transformation of Traditional Farmers Major Programs for Farmers Group Farming Project Permanent Food Production Park Project Transformation of Farmers’ Association Transformation of coconut Smallholders 10 Tan Paddy Project Malaysian Farm Accreditation Scheme Contract Farming Farm Mechanization Program Major Livestock Programs Cattle Integration in Palm Oil Plantation Closed System for Chicken Rearing Cattle feedlot system Malaysian Livestock Accreditation Scheme Contract Farming Major Programs for Fishermen Fund for Fishermen Transformation of National Fisherman’s Association Malaysian Aqua Farm Certification Scheme Contract Farming

- 51. Sectoral Transformation Development based on zoning/cluster : Increasing productivity Enhancing efficiency Promoting down stream activities Promoting integrated development AQUACULTURE INDUSTRIAL ZONE CROP ZONING PRODUCTION ZONES FOR LIVESTOCK TARGET AREA CONCENTRATION

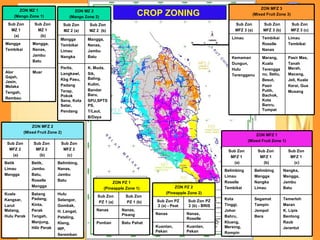

- 52. CROP ZONING ZON MFZ 1 (Mixed Fruit Zone 1) Sub Zon MFZ 1 (a) Sub Zon MFZ 1 (b) Sub Zon MFZ 1 (c) Belimbing Limau Roselle Tembikai Belimbing Mangga Nangka Limau Nangka, Mangga, Jambu Batu Kota Tinggi, Johor Bahru, Kluang, Mersing, Rompin Segamat Tampin Jempol Bera Temerloh Maran K. Lipis Bentong Raub Jerantut ZON MFZ 2 (Mixed Fruit Zone 2) Sub Zon MFZ 2 (a) Sub Zon MFZ 2 (b) Sub Zon MFZ 2 (c) Betik Limau Mangga Betik, Jambu Batu, Roselle Mangga Belimbing, Nanas, Jambu Batu Kuala Kangsar, Larut Matang, Hulu Perak Batang Padang, Kinta, Perak Tengah, Manjung, Hilir Perak Hulu Selangor, Gombak, H. Langat, Petaling, Klang, WP, Seremban ZON MFZ 3 (Mixed Fruit Zone 3) Sub Zon MFZ 3 (a) Sub Zon MFZ 3 (b) Sub Zon MFZ 3 (c) Limau Tembikai Roselle Nanas Limau Tembikai Kemaman Dungun, Hulu Terengganu Marang, Kuala Terengganu, Setiu, Besut, Pasir Putih, Bachok, Kota Banru, Tumpat Pasir Mas, Tanah Merah, Macang, Jeli, Kuala Kerai, Gua Musang ZON MZ 1 (Mango Zone 1) Sub Zon MZ 1 (a) Sub Zon MZ 1 (b) Mangga Tembikai Mangga, Nanas, Jambu Batu Alor Gajah, Jasin, Melaka Tengah, Rembau Muar ZON MZ 2 (Mango Zone 2) Sub Zon MZ 2 (a) Sub Zon MZ 2 (b) Mangga Tembikai Limau Nangka Mangga, Nanas, Jambu Batu Perlis, Langkawi, Kbg Pasu, Padang Terap, Pokok Sena, Kota Setar, Pendang K. Muda, Sik, Baling, Kulim, Bandar Baru, SPU,SPTSPS, T/Laut, B/Daya ZON PZ 1 (Pineapple Zone 1) Sub Zon PZ 1 (a) Sub Zon PZ 1 (b) Nanas Nanas, Pisang Pontian Batu Pahat ZON PZ 2 (Pineapple Zone 2) Sub Zon PZ 2 (a) - Peat Sub Zon PZ 2 (b) - BRIS Nanas Nanas, Roselle Kuantan, Pekan Kuantan, Pekan

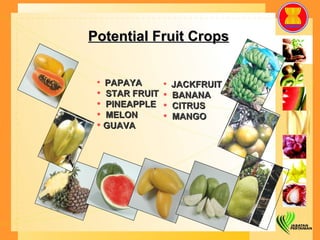

- 53. PAPAYA STAR FRUIT PINEAPPLE MELON GUAVA JACKFRUIT BANANA CITRUS MANGO Potential Fruit Crops

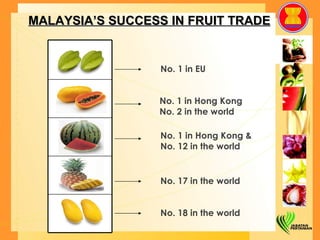

- 54. No. 1 in EU No. 1 in Hong Kong No. 2 in the world No. 1 in Hong Kong & No. 12 in the world No. 17 in the world No. 18 in the world MALAYSIA’S SUCCESS IN FRUIT TRADE

- 55. Sectoral Transformation Zoning/Cluster based development supported with activities, such as : Good Agricultural Practice Certification, Accreditation Schemes & Malaysia’s Best standardisation, commercialisation & transfer of technology Skilled training Supply – demand matching Sustainable agricultural development Pest/disease control

- 56. Sectoral Transformation Agro-based industry clusters: Meat based industry Fish based industry Fruit based industry Vegetables based industry Rice based industry Herbs based industry Coconut based industry

- 57. Sectoral Transformation Promoting private sector investment : Modern Farm Project Incubation centre Offering more attractive fiscal and non-fiscal incentive facilities Providing information as guidance to private sector investment Promoting large scale involvement of GLCs Offering more attractive financial schemes Centralized information centre by AGRI FOOD Business Development Centre (BDC)

- 58. Horizontal/Vertical Transformation Food Processing/ value-added activities : “ Winning Products ” Program 4 optional categories Sauce Snack Chilled Snack Drink & Beverages Package includes: Branding Quality Upgrading Design and Packaging Scheduled Production Aggressive promotion and advertisement

- 59. Brand names to promote SMI Products Branding Based On Quality And Food Safety

- 60. Horizontal/Vertical Transformation Supply chain activities: Infrastructure and marketing facilities Farm Collection Centre ICT facilities and post harvest handling equipments (grading, curing, storage, transportation, packaging and labeling) Information on market and extension Improvement to delivery process

- 61. Consumers Distributors Farmers Dist/collection centre Supermarket/ Hypermarket/ Retailers Processors Processed products S u p p l y C ha i n Management (SCM) Fresh produce PPL Receiving orders FAMA Input procurement Farm management Collection & post harvest Scheduled planting Delivery TESCO Giant Lifestyle Carrefour Billion PizzaHut Makro INTEGRATED SUPPLY CHAIN (DC) Chui Chak Selayang Puchong Tangkak Bkt. Mertajam Melaka Johor Bahru DC BDC FAMAX/AgricX

- 63. Thank you