Allowable Remuneration-Salary to Directors of a Company.pptx

- 1. Allowable Remuneration/Salary to Directors of a Company

- 2. One of the most thought-out and heatedly discussed issues in corporate governance has always been remuneration of Executive and Non-Executive Directors. The topic has become more important as it involves the cash outflow from the company, the calculation of net profits, disclosures to Shareholders, the approval of Directors, Shareholders, and the Remuneration Committee. Before knowing about remuneration to Directors first we will talk about Director and its types. Directors are members of the group known as the Board of Directors, who are responsible for charge of overseeing, managing, and guiding a company’s operations. Managing Director – A managing director is a director who has been entrusted with substantial management powers of a company by virtue of the company’s articles, an agreement with the company, a resolution passed in the company general meeting, or by the Board of Directors. Executive Director – An Executive Director is the company’s full-time working Director. They are in charge of the company’s affairs and are held to a higher standard. They must be diligent and cautious in all of their dealings.

- 3. Executive Director – An Executive Director is the company’s full-time working Director. They are in charge of the company’s affairs and are held to a higher standard. They must be diligent and cautious in all of their dealings. Non- executive Director – A Non-Executive Director is not involved in the day-to-day operations of the company. They might take part in the planning or policy-making process and challenge the executive directors to make decisions that are best for the company. Directors Salary vs. Remuneration: Salary is a subcategory of remuneration. A salary is a fixed amount of money paid to an employee on a regular basis; this amount is fixed and agreed upon by both the Employee and the Employer. “Remuneration” is a method of compensating a person for services rendered to a company. It refers to any money or equivalent given to anyone in exchange for services rendered. It includes perquisites as defined by the Income-tax Act of 1961. A director must be aware of the managerial remuneration authorized by Companies Act, 2013. Both a private limited company and a public limited company are required to follow regulations regarding the payment of managerial remuneration.

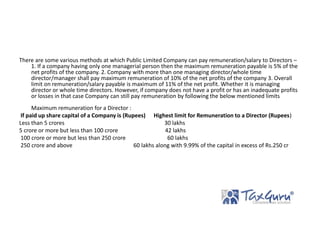

- 4. There are some various methods at which Public Limited Company can pay remuneration/salary to Directors – 1. If a company having only one managerial person then the maximum remuneration payable is 5% of the net profits of the company. 2. Company with more than one managing director/whole time director/manager shall pay maximum remuneration of 10% of the net profits of the company 3. Overall limit on remuneration/salary payable is maximum of 11% of the net profit. Whether it is managing director or whole time directors. However, if company does not have a profit or has an inadequate profits or losses in that case Company can still pay remuneration by following the below mentioned limits Maximum remuneration for a Director : If paid up share capital of a Company is (Rupees) Highest limit for Remuneration to a Director (Rupees) Less than 5 crores 30 lakhs 5 crore or more but less than 100 crore 42 lakhs 100 crore or more but less than 250 crore 60 lakhs 250 crore and above 60 lakhs along with 9.99% of the capital in excess of Rs.250 cr

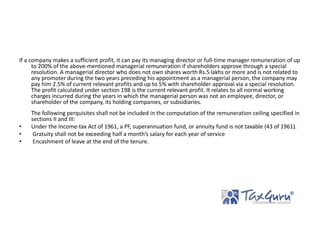

- 5. If a company makes a sufficient profit, it can pay its managing director or full-time manager remuneration of up to 200% of the above-mentioned managerial remuneration if shareholders approve through a special resolution. A managerial director who does not own shares worth Rs.5 lakhs or more and is not related to any promoter during the two years preceding his appointment as a managerial person, the company may pay him 2.5% of current relevant profits and up to 5% with shareholder approval via a special resolution. The profit calculated under section 198 is the current relevant profit. It relates to all normal working charges incurred during the years in which the managerial person was not an employee, director, or shareholder of the company, its holding companies, or subsidiaries. The following perquisites shall not be included in the computation of the remuneration ceiling specified in sections II and III: • Under the Income-tax Act of 1961, a PF, superannuation fund, or annuity fund is not taxable (43 of 1961). • Gratuity shall not be exceeding half a month’s salary for each year of service • Encashment of leave at the end of the tenure.

- 6. Any contribution made to a PF (Provident fund), superannuation fund, or annuity fund that exceeds the tax-deductible limits under the Internal Revenue Code of 1961 is not to be counted toward determining managerial compensation, according to clause (a). Whether there will be a profit or not. Section 197 applies only to Public Limited Companies and not to Private Limited Companies. Therefore, Private Limited Companies are allowed to pay remuneration at any rate without any limit whether there is adequacy or inadequacy of profits. Penalty for non-compliance If any person makes any default in complying with the provisions of section 197, he shall be liable to a penalty of one lakh rupees and if any default has been made by a company, the company shall be liable to a penalty of five lakh rupees. Tags: Companies Act, Companies Act 2013 Read more at: https://taxguru.in/company-law/allowable-remuneration-salary-directors-company.html Copyright © Taxguru.in